As reported on Wednesday at the Institute for Supply Management (ISM), the purchasing managers' index (PMI) for the US manufacturing sector in November rose to 61.1 (against 60.8 in October and the forecast of 61.0). The index is well above 50.0 points, which separates the zone of growth in activity from the zone of its decline, and signals a strong increase in manufacturing activity, while companies reported the first signs of easing tensions in supplies. Demand for goods also remained strong in November, with the ISM manufacturing new orders rising to 61.5 from 59.8 in October. At the same time, the ISM employment index rose to 53.3 from 52.0 in October.

These very strong values, indicating the continued improvement in the state of the American economy, in particular its manufacturing sector, came out after the positive employment data from the ADP, according to which the rate of creation of new jobs in the US private sector in November remained quite high. As reported in ADP, the number of jobs in the private sector in November increased by +534,000 (against the forecast of +525,000 and the previous value of +570,000). "The labor market continued to recover in the past month, despite all the difficulties", - commented in the ADP.

Now market participants will wait for the publication on Friday of the official report of the US Department of Labor on the number of jobs outside of agriculture for November. ADP data may differ significantly from Labor Department data, however, they are often viewed as a harbinger of official data, and strong ADP figures give hope for an equally strong US Department of Labor report: Economists expect +550,000 job growth (vs. +531,000 in October) and a decrease in the unemployment rate to 4.5% (from 4.6% in October).

The dollar may receive additional support, reacting to the publication of strong macroeconomic statistics, which may testify in favor of the decision on a more rapid tightening of monetary policy by the Fed.

The upward momentum of the dollar intensified after the speech by the head of the Fed Jerome Powell in Congress last Tuesday. Powell acknowledged that inflation in the US should not be considered a temporary phenomenon now, and to tame its further growth, it is highly likely that more active action by the Fed will be required. In this regard, Powell considers it necessary to accelerate the phasing out of economy stimulating. "The economy is in very good shape, inflationary pressures are high, therefore, in my opinion, it is advisable to consider rescheduling (plans) for curtailing the purchase of assets, which we actually announced at the November meeting, for a few months earlier", Powell said.

Meanwhile, the Organization for Economic Cooperation and Development (OECD) in a regular report said that inflation in the United States in 2022 will be 4.4%, not 3.1%, as economists of the organization expected in September.

If after the December meeting, which will be held on December 14-15, Fed leaders accelerate the pace of reduction in asset purchases, for example, to $ 30 billion a month, then the QE program may be completed by March, which will increase the likelihood of an increase in interest rates in the first half of next year. And this prospect creates the preconditions for further strengthening of the dollar.

Unexpected risks from a new, more contagious strain of the omicron coronavirus found in South Africa will also help support demand for the dollar as a defensive asset.

Tomorrow, simultaneously with the publication of the report of the US Department of Labor (at 13:30 GMT), data on the labor market will be published by Statistics Canada. Unemployment has risen in Canada in recent months, including amid massive business closings due to coronavirus and layoffs. Unemployment rose from the usual 5.6% - 5.7% to 7.8% in March and already up to 13.7% in May 2020. If unemployment continues to rise, the Canadian dollar will decline. If the data is better than the previous value, the Canadian dollar will strengthen. A decrease in the unemployment rate is a positive factor for CAD, an increase in unemployment is a negative factor. In August, unemployment was at 7.1%, and in October 6.7% (versus 7.5% in July, 7.8% in June, 8.2% in May, 8.1% in April). According to the forecast, unemployment in Canada is expected to drop to 6.6% in November, and the number of employed increased by another +35,000.

This is moderately positive data for the CAD, whose quotes are likely to grow supported by the resumed growth in oil prices after their strong fall in the previous 4 trading sessions. It looks like fears about a new strain of coronavirus have eased.

Canada is the largest exporter of oil, and the share of oil and oil products in the country's exports is approximately 22%. Despite some uncertainty in the oil market due to the coronavirus, many leading economists predict a further increase in energy prices (coal, gas, oil), including due to expectations of a cold winter and rush demand in the gas market.

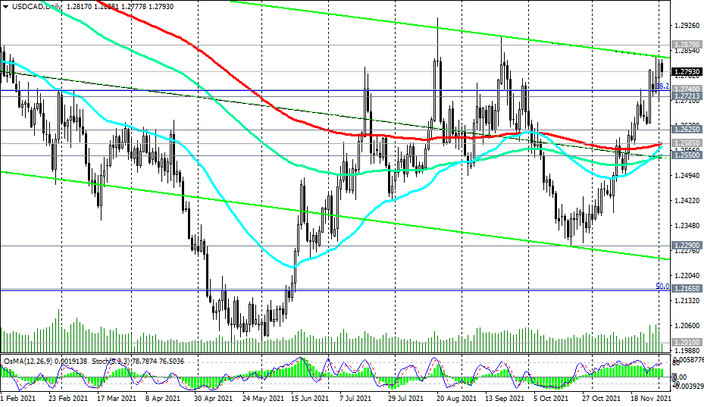

Thus, on Friday at 13:30 (GMT) a sharp increase in volatility is expected in the financial markets and, above all, in the USD / CAD pair. If the official data of the US Department of Labor turns out to be disappointing, then we should expect a weakening of the US dollar and a decline in USD / CAD.