On Tuesday, the growth of US Treasury yields continues. At the time of publication of this article, the yield on the US 10-year bonds is 1.525% versus the 1.491% mark at the close of the market yesterday, corresponding to the levels of 3 months ago. This is already the 6th week of continuous growth in the yield of 10-year government bonds, which, as you know, grows with a decrease in their quotations. Longer-term 30-year yields have reached levels above the psychologically important 2% mark.

Market participants continue to analyze signals from the Fed about its readiness to begin phasing out the program to buy Treasury bonds and mortgage-backed securities, counting on the fact that the US central bank will announce in November that it will begin cutting its bond buyback program by $ 120 billion.

Economists forecast that the first increase in interest rates from the current 0.25% by a few basis points will occur towards the end of 2022. They believe that by this time the American economy should fully recover from the consequences of the coronavirus pandemic, and inflation should consolidate at about 2% per year. At the same time, about half of the Fed's executives believe that by the end of 2023, rates will need to be raised by 1 percentage point from current levels and by another three-quarters of a percentage point in 2024.

The growth in government bond yields and the prospect of raising interest rates increase the attractiveness of the US dollar in relation to its main competitors.

New York Fed chief and FOMC member John Williams said on Monday that the time for a cut in asset purchases by the central bank is approaching, although he made it clear that there is still a long way to go before raising interest rates. "It is clear that we have made substantial further progress towards our inflation target", and "there is very much progress towards peak employment. If the economy improves as I expect, a slowdown in asset purchases will soon be justified", Williams said.

In turn, the dollar received additional support on Monday, when positive data on the dynamics of orders for durable goods in the United States was published, according to which, the volume of orders in August increased by 1.8% (after rising by 0.5% in July and vs. forecast +0.7%). Orders for capital goods excluding the defense and aviation sectors rose by 0.5% (versus the forecast of +0.4% and growth of 0.3% in July). This is the strongest growth in indicators since May.

Today, investors expect Fed Chairman Jerome Powell to address Congress at 14:00 (GMT). The text of his speech, which became available to journalists, expresses Powell's opinion that inflation in the United States is likely to remain elevated in the coming months and then decline. Powell will also likely repeat the statements he made last week following the Fed meeting, when the central bank signaled its intention to begin revising its soft monetary policy at a meeting scheduled for November 2-3.

In addition, at 13:00 and 14:00 (GMT) from the United States will come statistics on the level of consumer confidence in September, as well as July data on the dynamics of house prices. With the growth of indicators, the dollar will receive additional short-term support.

Meanwhile, market participants monitoring the dynamics of the euro and the EUR / USD pair will pay attention to the speech of the head of the ECB Christine Lagarde, which is scheduled to start at 12:00 (GMT). At the economic forum in Sintra, Christine Lagarde will give opening remarks, among other things, possibly raising the issue of the central bank's attitude to inflation.

Many economists expect headline inflation in the Eurozone to be 3.3% in September and core inflation to 1.9%. On Friday, Eurostat is to publish preliminary data on inflation in the Eurozone for September. Today, Christine Lagarde is likely to characterize the increased inflation as temporary.

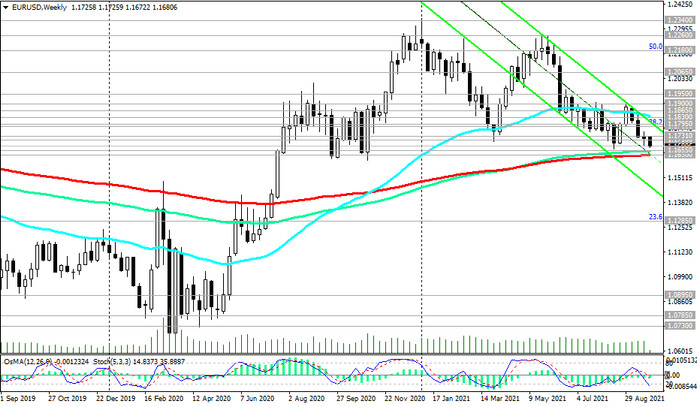

Amid the soft monetary policy of the European Central Bank, the euro will remain vulnerable to the dollar amid rising US Treasury yields and anticipating the soon start of the Fed's QE program. EUR / USD is declining today for the third day and for the 4th week in a row, being primarily under the pressure of the strengthening dollar. In this situation, the EUR / USD pair may soon decline below the key long-term support 1.1630 (see Technical Analysis and Trading Recommendations), which will mean its transition to the long-term bear market zone.