According to the minutes of the March meeting published yesterday evening, the Fed leaders are largely unanimous in the opinion that it is necessary to continue to support the economy by maintaining ultra-low interest rates and making large monthly bond purchases. During the meeting, held March 16-17, they said they still expect interest rates to remain near zero until the end of 2023, and did not express their readiness to curtail the bond purchase program.

"The current leading indication of the Committee (on open market operations) regarding the federal funds rate and asset purchases is beneficial to the economy", the minutes say.

Today at 16:00 (GMT) the speech of the head of the FRS Jerome Powell will begin. At a press conference after the March meeting, Powell said that "the economic recovery is uneven and far from over, and the road ahead remains uncertain", noting that current "monetary policy will continue to provide strong support to the economy until its recovery is complete".

Powell is likely to reaffirm the commitment of the Fed leadership to continue the current policy today.

Other Fed leaders have also previously confirmed this position in their statements. Thus, the president of the Federal Reserve Bank of Chicago, Charles Evans, said last Wednesday that "monetary policy will remain unchanged for some time". His colleague, President of the Federal Reserve Bank of Dallas, Robert Kaplan, said on Tuesday that he agreed "with the direction of monetary policy in general", stressing that "the crisis has not yet been overcome".

Fed officials continue to argue that interest rates will not rise until full employment is achieved, inflation will not accelerate to 2%, and inflation forecasts will not assume that it will linger at moderately over 2% for a while. Asset purchases will not shrink until central bank officials see "significant additional progress" towards these goals.

Earlier Powell promised that the Fed would give early warning of the possible timing of the start of the rollback of bond purchases, which now amount to $ 120 billion a month.

At the same time, the heads of the FRS did not specify what level of unemployment corresponds to their idea of full employment (in March it was 6%, and we can talk about unemployment 4% -4.5%). At the same time, all of them, noting the improvement in economic prospects, say something like the following: "there is reason to be optimistic about the future".

In particular, a new government stimulus plan worth $ 1.9 trillion, which acquired the status of law on March 11, pushed the Fed leaders to raise forecasts for inflation and growth of the American economy.

This huge amount, which will soon flow into the financial system, is placing an additional significant burden on the federal budget, increasing the already huge US national debt, accelerating inflation.

And since many market participants are focused on the future, they can already include in their plans earlier dates for the start of tightening the Fed's policy, especially since the Fed leaders still do not pay significant attention to the growth of US government bond yields. This growth is known to be related to the strengthening of their sales. If this process (growth in government bond yields) continues, and the Fed still does not intervene in it or cannot reverse it with its purchases, which currently amount to $ 120 billion a month, then the dollar's downtrend may be broken. Moreover, other major world central banks also adhere to super-soft policies, keeping their interest rates near zero levels.

At the start of the European session, the DXY dollar index declines after hitting a local 5-month high at 93.47 last week. DXY futures are traded close to 92.42 mark as of this writing, although US 10-year yields are holding around 1.650%, near 15-month highs.

Economists and market participants continue to assess the prospects for the stock market and the dollar, and in this assessment, on the one hand, there are expectations of accelerated growth of the American economy and the Fed's soft policy, and on the other, accelerated inflation in the United States and the growth of federal debt, given the huge new infrastructure spending.

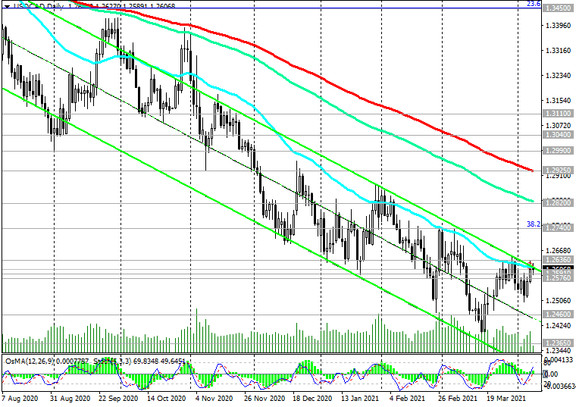

In addition to the pound, the Canadian dollar also showed weakness against the US dollar this week.

Today the publication of important news on Canada is not planned, but tomorrow market participants trading the Canadian dollar and the USD / CAD pair will pay attention to the publication at 12:30 (GMT) of the most important data from the Canadian labor market. In 2020, unemployment in Canada rose from the usual 5.6% - 5.7% for the country to 7.8% in March and already up to 13.7% in May amid massive closures due to coronavirus and layoffs. If unemployment continues to rise, the Canadian dollar will decline. A decrease in the unemployment rate is a positive factor for CAD, an increase in unemployment is a negative factor. Canadian unemployment is expected to be 8% in March (versus 8.2% in February, 9.4% in January, 8.8% in December, 8.6% in November), and employment rose by 100,000 humans.

If the data turns out to be better than the previous value and forecast, then the Canadian dollar will strengthen, including in the USD / CAD pair. The data below the forecast will put pressure on the CAD. Its quotes are also strongly influenced by the dynamics of oil prices, and so far, they do not show signs of further growth, having stabilized at support levels.